Imagine saving $150 a month on the same home, just because rates dropped. Read on to see how much home could you afford at today’s mortgage rates.

Imagine saving $150 a month on the same home, just because rates dropped. Read on to see how much home could you afford at today’s mortgage rates.

That’s exactly what’s happening now, thanks to mortgage rates dropping to their lowest point in 11 months. That drop means homebuyers in Huntsville have more purchasing power today than they’ve had in nearly a year.

Let’s dive in.

What Happens When Mortgage Rates Drop?

Mortgage rates work like a price tag on your loan. When rates are high, borrowing money costs more each month. When they drop, even by a small percentage, your monthly payment shrinks.

That lower payment means one of two things:

-

You spend less each month for the same home.

-

You buy more home for the same monthly budget.

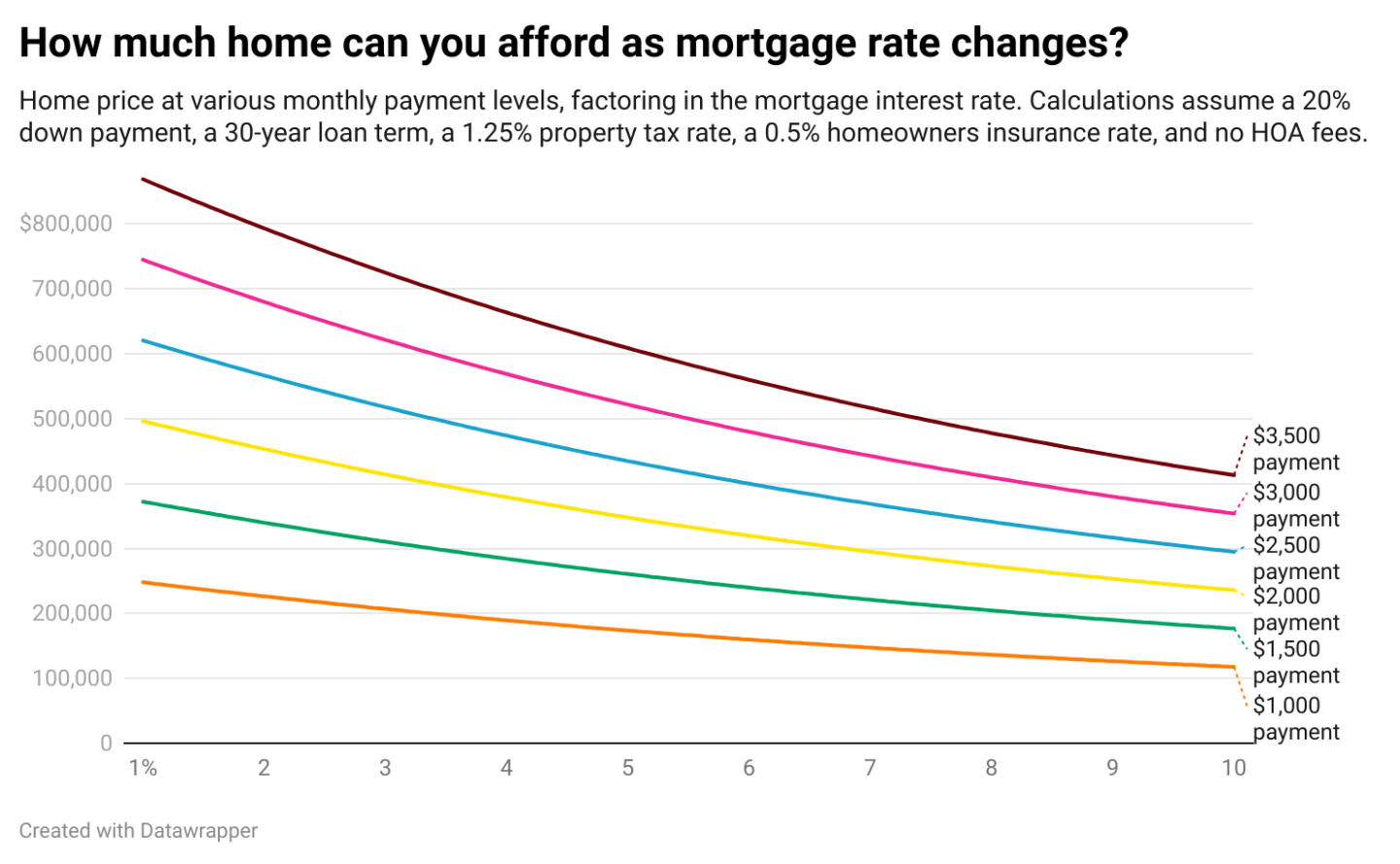

Let’s look at an example of a buyer with a $3,000 monthly housing budget.

In June, when rates averaged 6.9% a buyer could afford about $446,000, assuming a 20% down payment on a 30-year mortgage.

A couple of weeks ago, when rates were closer to 6.5%, that same buyer could afford a $460,500 home.

And now that rates have a new 2025 low of 6.27%? That buyer can afford a home worth $468,000.

In other words, buyers have gained $7,500 in purchasing power in the past week alone and a total of $22,000 in just three months.

Monthly Savings Add Up Fast

Here’s another way to look at this:

The median U.S. home costs about $444,000. In June, the monthly mortgage payment would have been about $2,624 for a median-priced home.

Today, the monthly mortgage payment for that home comes in at $2,481—a savings of roughly $150 every month. Over the life of a loan, that’s tens of thousands of dollars saved.

Now, let’s look at an example here in Huntsville, where the median home price is currently $330,000.

Let’s look at the math:

- Monthly payment for a median-priced home in Huntsville at 6.29%: $2,040

- Monthly payment at 6.5%: $2,086

- Monthly savings: $45

Those monthly savings on housing could help in a number of ways:

- Building a “rainy day fund”

- Paying off higher-interest debt more quickly

- Investing for retirement

- Saving for a vacation or a bucket list adventure

- Saving for holiday spending (gifts, travel, decorating)

Is This Your Window?

Mortgage rates don’t typically fall this low without good reason. Recent economic data has shifted the outlook, and buyers are in a unique position.

Lower rates don’t just improve affordability; they also create new opportunities in the housing market.

Families

Families  If your home didn’t sell the first time, or you’re thinking about listing soon, there’s one question that can make or break your entire experience:

If your home didn’t sell the first time, or you’re thinking about listing soon, there’s one question that can make or break your entire experience: When it comes to selling a home in

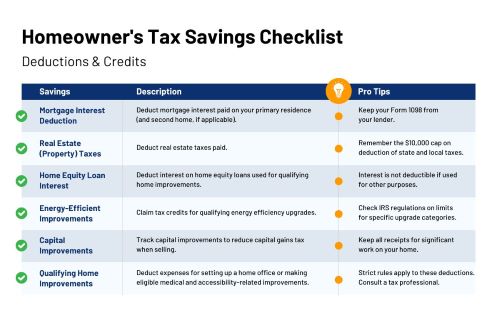

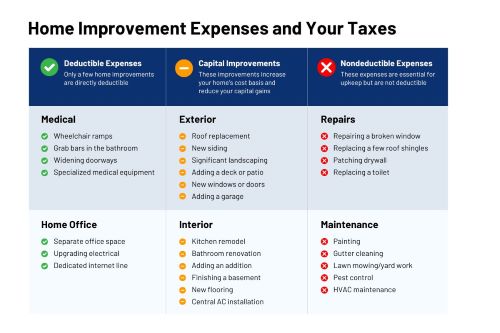

When it comes to selling a home in  Tax season. Just the words can send shivers down your spine. But if you’re a homeowner, there’s a silver lining: homeowner tax deductions in 2025 can lead to potential savings! Read on to learn about home-related tax deductions that may help you save.

Tax season. Just the words can send shivers down your spine. But if you’re a homeowner, there’s a silver lining: homeowner tax deductions in 2025 can lead to potential savings! Read on to learn about home-related tax deductions that may help you save.